Not afraid of the tariff storm, Overlord Tea Girl is about to land in U.S. stocks. There are new strategies at the end of the articleˇ

It just happens that many people have come to ask recently. Today, I will use the topic to talk to you about how to make new U.S. stocks.

The moat of the Overlord Tea Lady: high expansion, low store closure rate, and strong individual profitability

Let's briefly introduce Bawang Tea Girl first: The company was founded in 2017 and is the largest, fastest-growing and most popular high-end freshly made tea beverage brand in China.Many people may only drink it, but they don't know much about the company's financial situation.Brother Zhang Biao studied it for a while and was startled.

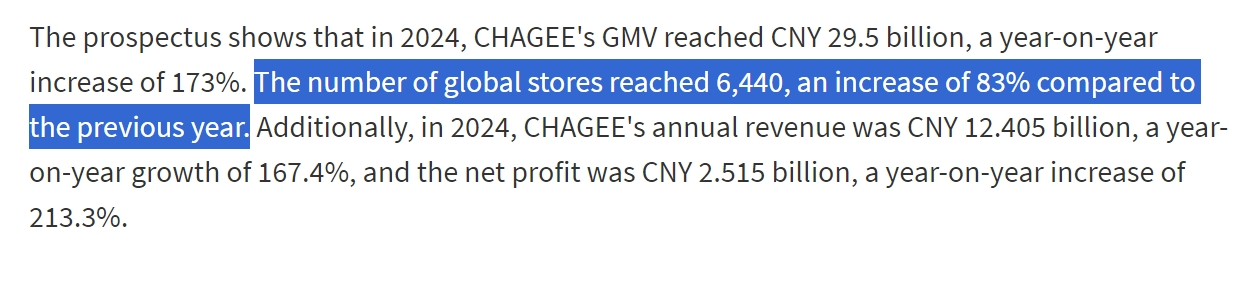

From the perspective of financial performance, the growth of Bawang Tea Lady can be regarded as an industry benchmark.In 2024, its revenue will reach 12.405 billion yuan, a year-on-year surge of 167%, net profit will be 2.515 billion yuan, and net profit margin will reach 20.3%, which is very eye-catching.

As of the end of 2024, the number of stores in the world has reached 6,440, an increase of 83% from 3,511 in 2023, and the store closure rate is only 1.5%, far below the industry average-high expansion is not scary, but such a low store closure rate is scary.Chaji adopts a mixed expansion strategy of "direct sales + franchising", which not only ensures the consistency of brand tonality, but also uses the network of franchisees to achieve rapid sinking, forming differentiated competition with Mixue Ice City's path.

In addition to high expansion and low store closures, every store of Bawang Tea Lady has strong individual combat capabilities.According to the prospectus, the average annual revenue of Chaji's single store is 1.92 million yuan (based on total revenue of 12.4 billion yuan), which is significantly higher than Guming's 1 million yuan/store.

Every store adopts extremely standardized operations: the top three single products contribute 60% of revenue, the inventory turnover is only 5.3 days, and the automated cup delivery system achieves 40 seconds of delivery (as of August 2024, the sales volume of "Bo Ya Juexian" exceeds 600 million); In terms of pricing strategy, the 15-20 yuan pricing strategy avoids the positive competition between Mixue Ice City (8 yuan) and Xi Tea (20+ yuan). Currently, Bawang Chaji has firmly occupied a 20.3% share of high-end freshly made tea drinks.

Such a store is exemplary in terms of finance and operation, and it will be a matter of time before it launches into the primary market.

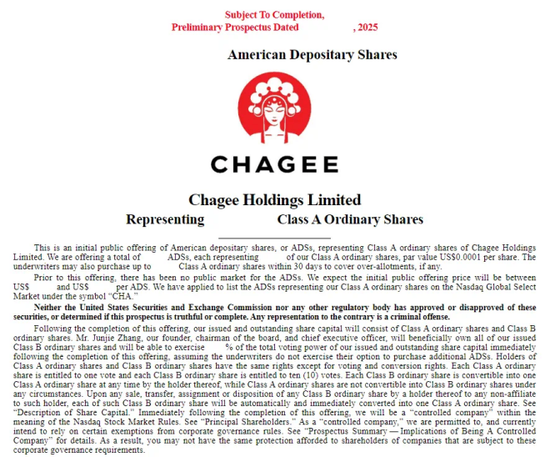

The planned fundraising of US$411 million will become the "first share of new tea drinks and U.S. stocks."

Let's take a look at the prospectus again.

According to SEC documents, this time the Overlord Tea Lady plans to issue 14.68 million American Depositary Shares (ADSs) at a price of US$26 -28 per share, raising a total of US$411 million.

Based on the upper limit of the issue price range, its valuation will climb to US$3.3 billion. This figure not only far exceeds Naixue's current market value of approximately HK$8 billion (approximately US$1.03 billion), but also places it among the world's freshly made tea brands. The first echelon of valuation.

The underwriting team is also luxurious.The IPO is jointly underwritten by Citigroup, Morgan Stanley, China International International Capital Corporation and Deutsche Bank, and is expected to be launched on the Nasdaq Global Select Market with the ticker symbol "CHA".

Everyone may be curious, why did Overlord Tea Lady choose to list on U.S. stocks instead of Hong Kong stocks?Mainly because of the consideration of valuation premiums.The U.S. capital market usually gives high-growth consumer brands a higher price-to-sales ratio (P/S), while Bawang Tea Ji's GMV (total commodity transaction volume) in 2024 will reach 29.5 billion yuan, a year-on-year increase of 173%. This growth rate is sufficient to support its $3.3 billion valuation expectations.

Secondly, the plan to go to sea has been one of the focuses of Overlord Tea Lady in recent years.At present, it has more than 150 stores in Malaysia, Singapore and other places. It plans to add 1,000 - 1,500 stores in 2025, and plans to open its first store in the United States in Los Angeles, aiming at a global layout.From this perspective, landing in U.S. stocks is indeed better than Hong Kong stocks.

Valuation & New Strategies

Let's look at the valuation that everyone is most concerned about.

The P/E ratio of Bawang Tea Ji's IPO is about 15 times (based on a net profit of 2.515 billion yuan in 2024), which is significantly lower than 32 times for Mixue Ice City and 25 times for Guming, leaving a lot of water level for the market.

This valuation difference stems from its U.S. stock listing nature (the valuation discount of Chinese stocks) and the market's concerns about the slowdown in the growth of tea drinking tracks, but the horizontal comparison is still attractive.For example, if we compare Starbucks (the current dynamic PE is about 26 times), the value of tea lady will be repaired as high as 73%, which is very attractive.

Even if we don't look at PE and look at the price-to-sales ratio (PS) alone, the pricing of US$26 -28 is still low-the offering price range of US$26 -28 corresponds to a market value of US$3.0 - 3.3 billion.Based on the revenue of 12.4 billion yuan in 2024, the market sales rate (PS) of Bawang Chaji is only 0.24 times, which is significantly lower than the average of 0.5-0.8 times in the current tea beverage industry.

On a new level, unlike Hong Kong stocks, there are no statutory unified allocation rules for the issuance of new shares in the United States. It is up to the underwriters or distributors to decide how to allocate them to investors participating in the subscription of new shares.

Brother notes studied it and found that this time, the threshold for new securities firms for Overlord Tea Lady is higher, and some securities firms even require 800W capital verification.In contrast, Tiger, as an underwriter, is most likely to get on the bus (zero fee subscription).

_909447440_847.jpg)

Tiger has two rules for allocating new shares: try to get as much as possible, and get as much as you recognize-1. Try to allow as many investors participating in the subscription of new shares to win;2. Investors with larger subscriptions usually receive more shares than (or no less than) investors with smaller subscriptions.

Under optimistic scenarios, assuming that the number of stores increases to 7500 in 2025 and the revenue of single store rebounds to 1.8 million yuan, the annual revenue can reach 13.5 billion yuan (+8.8%), and the net profit is calculated based on a 20% net interest rate. 2.7 billion yuan, corresponding to about 12 times dynamic PE, and there is 66% room for growth if the valuation is restored to 20 times PE.

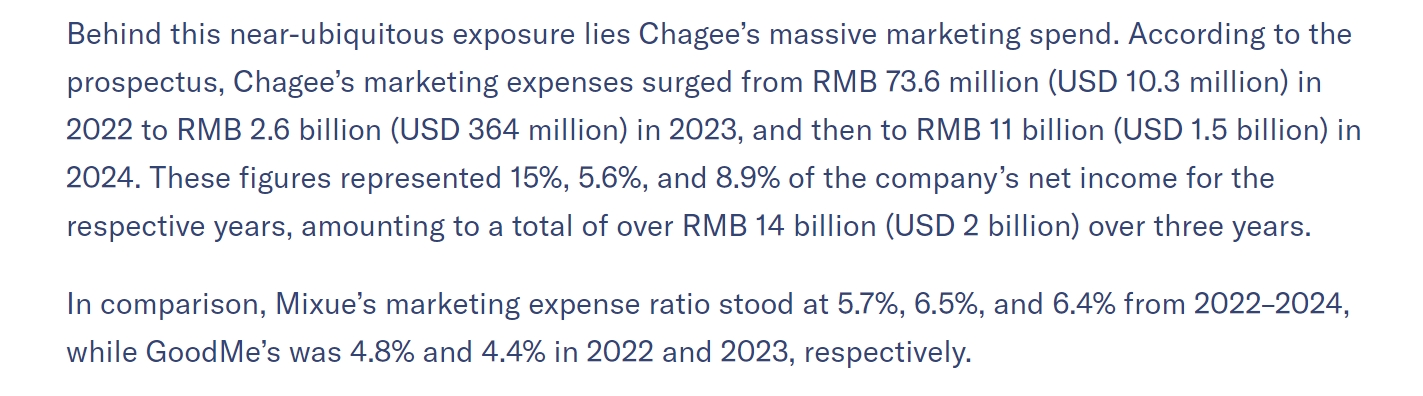

In terms of risks, everyone should pay attention to the rigid growth of Chaji's marketing expenses-advertising investment in 2024 is 1.1 billion yuan (accounting for 8.9% of revenue), but the brand's mentality has not yet established a moat, and it needs to continue to burn money to maintain its sound volume.

Secondly, there is the price war of tea drinks. Under the pessimistic scenario, if the revenue of a single store continues to fall to 1.5 million yuan/year, and the combined price war causes the net interest rate to be compressed to 15%, the net profit will be only 1.82 billion yuan. The current valuation The actual PE is 18 times, which loses the cost performance compared with Mixue Ice City.

Finally, there are some other subscription information.

● Minimum subscription: US$1,040 (50 shares-comprehensive account)

● Subscription deadline: 2025.04.16 19:00 (expected)

● Time to market: 2025.04.17 (expected)

Time is tight and tasks are heavy, so friends who want to get on the bus must hurry up ~

Recently, if there are new Hong Kong and U.S. stocks, or if you want to exchange accounts for Hong Kong and U.S. stocks, you can add a small WeChat exchange.

![[Pre-market Analysis of U.S. Stocks] Pre-market Keywords of the day (2025.10.14)](https://hawk-oss.hawkinsight.com//picture//202508/328687551_275.png?w=3840&q=100)

![[Intraday Analysis of U.S. Stocks] Finance and transfer of assets took over and pushed up. Daoqiongke companies were under pressure, and the index was weak. (2025.10.15)](https://hawk-oss.hawkinsight.com//picture//202508/328826217_1.png?w=3840&q=100)