NVIDIA Q2 revenue exceeds expectations, but Blackwell's hot sales cannot hide the gap in China

In the second quarter, Nvidia's core AI chip H20 failed to bring any revenue in China.

On August 27, Nvidia, the "chief leader" of artificial intelligence, announced its second quarter results report for the fiscal year 2026.

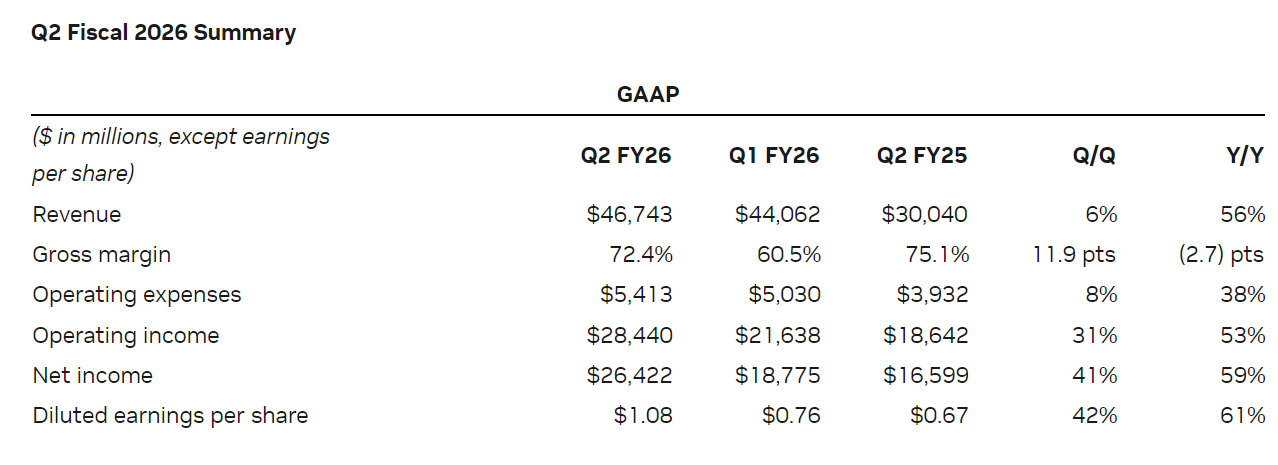

Data showed that during the reporting period, the company's revenue reached US$46.7 billion, a year-on-year increase of 56%, and net profit was also higher than Wall Street expectations.

Among them, Blackwell architecture chip shipments were strong, with a month-on-month increase of 17%. The game and AI PC businesses continued to be booming, and the professional visualization and automotive chip businesses also maintained double-digit growth.These sectors provide the company with a diversified growth curve.

However, what really determines market sentiment is still the data center business.This sector contributed more than 80% of revenue, but experienced a month-on-month decline of 1%. Among them, the H20 sales gap alone lowered revenue by US$4 billion.Nvidia admitted during the telephone conference that vacancies in the China market were the main cause of the drag.

According to the report, in the second quarter, Nvidia's core AI chip H20 was blank in China and failed to generate any revenue.

This is not simply a market issue, but a reflection of geopolitics.In the past year, the U.S. government has imposed multiple restrictions on the export of high-end AI chips to China.Although Huang Renxun sent an optimistic signal when he visited China in July, saying that he had obtained an export license, the financial report clearly pointed out that no H20 chips were delivered to China in the second quarter.

In other words, the license has not yet been converted into a physical order.The chief financial officer even emphasized that the US$54 billion revenue forecast for the third quarter did not take into account the possible revenue from the China market.

However, Nvidia has not given up its bet on China.

At the performance meeting, the CFO predicted that if geopolitical obstacles were lifted, China market could contribute US$2 billion to US$5 billion in H20 revenue in the next few quarters. Huang Renxun even bluntly said that China may bring US$50 billion in business opportunities this year, and hinted that the next generation Blackwell also has the opportunity to land in China.

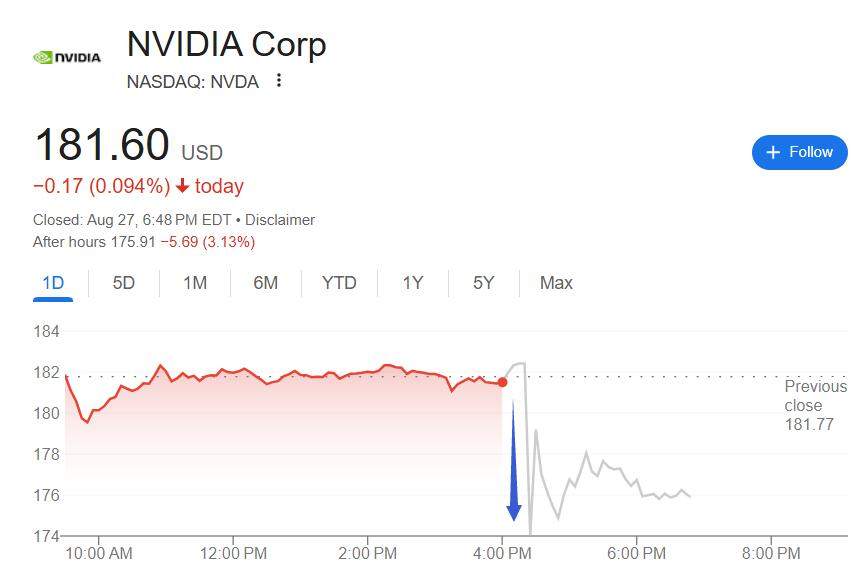

After the earnings report was announced, Nvidia's share price fluctuated sharply after hours, falling by 5%, but eventually narrowed to less than 2%.

Investors not only see the stability of the company's short-term earnings, but also worry about future growth's dependence on the continued persistence of AI capital expenditures and the possible ceiling effect of the absence of the China market.Analysts generally pointed out that Nvidia has entered a stage of "turning from wild to steady". Although its performance guidance is higher than the market consensus, it is difficult to reproduce the previous growth rate of 70% to 80%.

Against this background, the company launched a US$60 billion share repurchase authorization, which became an important signal of confidence.

In the first half of this year, Nvidia has repaid US$24.3 billion to shareholders through repurchase and dividends.The new repurchase amount is equivalent to nearly a quarter of the company's market value, meaning that even if growth slows, management will still have enough cash flow and profitability to support long-term commitments to shareholders.

From a more macro perspective, Nvidia's financial report reflects the structural contradictions in the development of the global AI industry.

On the one hand, the demand for AI infrastructure remains strong.Huang Renxun predicts that by 2030, the world will invest 3 to 4 trillion US dollars in building AI computing power, and Nvidia is expected to receive hundreds of billions of US dollars of this.There is little suspense about this long-term trend.

On the other hand, technology and markets are being receded by geopolitics.U.S. export controls and China's independent substitution have forced Nvidia to face the reality of "world division."For investors, the real risk is not the level of revenue in a single fiscal quarter, but whether Nvidia can remain co-existing and competitive in both systems.

Current signs show that the China market is accelerating the application substitution of domestic GPUs and AI chips.If this trend continues, Nvidia may not be able to regain its previous market share even if it returns to China.At the same time, the United States 'game over chip policy may also be further tightened, causing Nvidia's business in China to face repeated setbacks again.In other words, the absence of China's market is not just a short-term income gap, but is more likely to gradually evolve into a long-term strategic risk.

Despite this, Nvidia is still the most irreplaceable link in the AI industry chain.According to the analysis, whether it is large model training, cloud computing acceleration or game graphics rendering, Nvidia's technical barriers and ecological advantages still exist.

·Original

Disclaimer: The views in this article are from the original Creator and do not represent the views or position of Hawk Insight. The content of the article is for reference, communication and learning only, and does not constitute investment advice. If it involves copyright issues, please contact us for deletion.

![[Intraday Analysis of U.S. Stocks] Bulls return to temperature Technology and semiconductors lead gains in earnings and policy signals affect risk appetite (2025.10.21)](https://hawk-oss.hawkinsight.com//picture//202508/328826217_1.png?w=3840&q=100)

![[Pre-market Analysis of U.S. Stocks] Pre-market Keywords of the day (2025.10.21)](https://hawk-oss.hawkinsight.com//picture//202508/328687551_275.png?w=3840&q=100)