[After-hours Analysis of U.S. Stocks] Expectations for interest rate cuts fall, U.S. stocks pull back (2025.08.01)

Good financial reports from Meta and Microsoft once drove U.S. stocks higher. However, expectations for interest rate cuts fell after the release of inflation and employment data. Markets were worried that the United States would delay interest rate cuts. Coupled with the uncertainty of Trump's tariff policy, U.S. stocks eventually turned black.

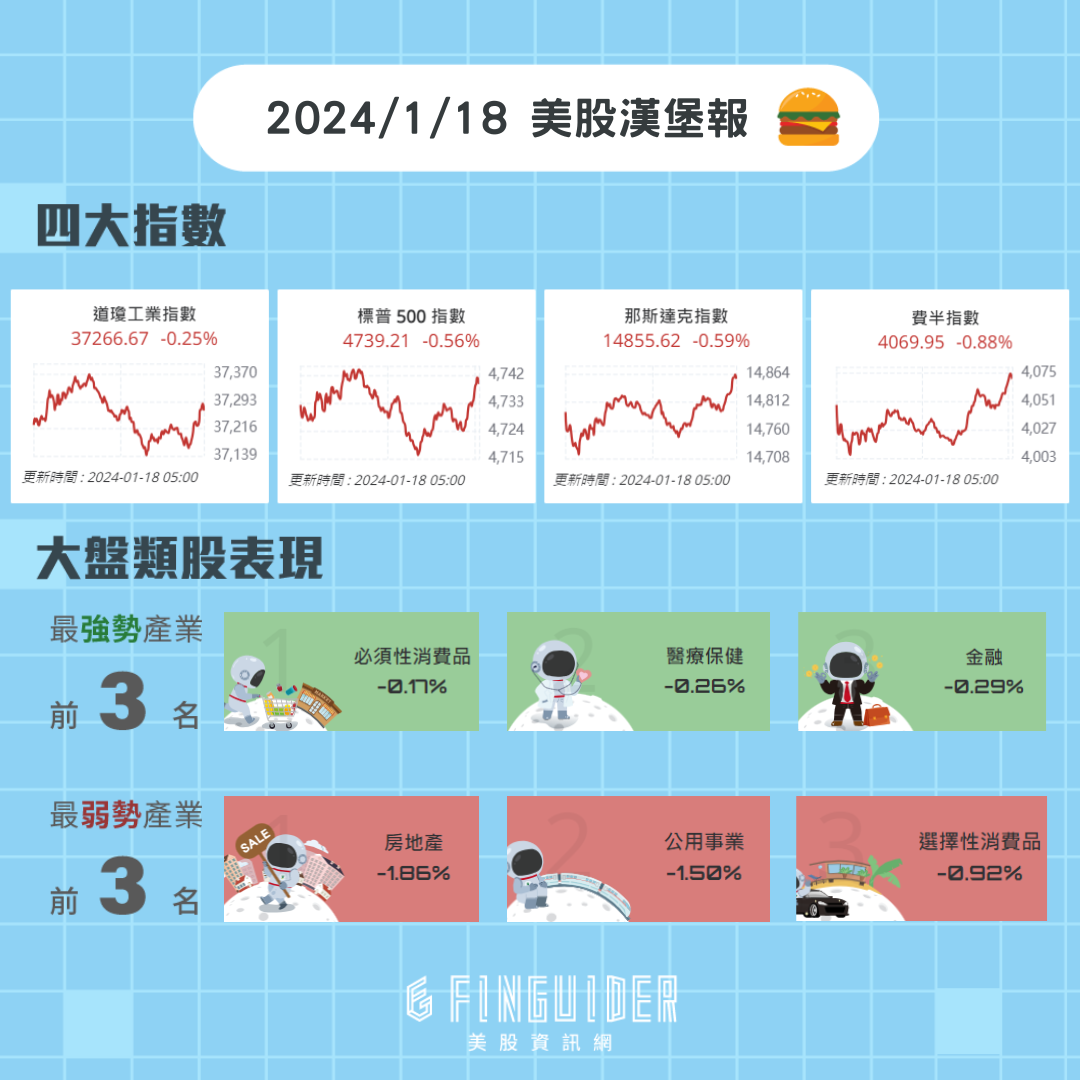

Market analysis

Market analysis

Quick view of financial report

Amazon's AWS cloud performance fell short of expectations, and pressure on profits caused stock prices to plummet

Amazon (AMZN) announced its second-quarter earnings report. Overall revenue and profit exceeded market expectations, with revenue reaching US$167.7 billion, a year-on-year increase of 13%, and earnings per share of US$1.68. However, its cloud business AWS grew by only 17.5%, and its gross profit margin fell to 32.9%. It appears relatively weak in the face of higher growth in Microsoft Azure and Google Cloud. Although AWS remains the core of Amazon's profits, the squeeze in gross profit and the gap in market expectations caused after-hours stock prices to plummet by more than 7%.

In addition, although Amazon is actively investing in AI infrastructure, it has not yet shown a leading edge in the development of generative AI applications and models. Investors are still holding a wait-and-see attitude towards whether its tens of billions of dollars in AI spending is effective.

云端业务成长不及竞争对手

AWS营收达308.7亿美元,年增17.5%,但明显落后微软Azure(+39%)与Google Cloud(+32%);获利贡献占比仍高达60%,但毛利率下滑引发市场担忧。AI投资巨大但回报不明

亚马逊预估全年AI与云端基础设施支出达1,180亿美元,高于市场预期的1,000亿,CEO Jassy虽强调AI进展改善效率与体验,但缺乏亮眼AI产品仍是疑虑。营运展望偏保守

第三季营收预估为1,740亿至1,795亿美元,高于预期,但营业利益预测区间为155亿至205亿美元,略低于市场共识的194.5亿,引发利润压缩忧虑。广告与零售维持双位数成长

广告营收达157亿美元、年增23%,线上商店营收增至615亿美元;这两项业务持续稳健,部分对冲AWS压力。关税影响尚未显现

Jassy指出目前关税对需求与价格影响有限,但未来仍存不确定性,特别是中国供应链仍可能受美国政策扰动。

Apple's Q3 revenue hits the largest growth in nearly four years, iPhone sales drive results, AI and tariffs become the focus

Apple (AAPL) announced its third-quarter 2025 financial report, with total revenue reaching US$94.04 billion, an increase of nearly 10% year-on-year, the largest single-quarter growth since December 2021. iPhone sales grew strongly by 13.5%, driving overall performance to exceed market expectations. Despite rising tariff pressure and questioning AI progress, CEO Cook made it clear that he would significantly increase investment in artificial intelligence and did not rule out further mergers and acquisitions. The China market has also returned to growth stimulated by subsidies, demonstrating the potential for market rebound.

Apple expects revenue to maintain mid-to-high single-digit growth in the next quarter, indicating that the company's fundamentals are solid, but it will still face multiple pressures from tariff policies, AI competition and European regulatory challenges in the future.

iPhone与Mac销售强劲

iPhone销售年增13.5%,达445.8亿美元,为成长主因;Mac销售亦大增近15%,反映MacBook Air更新效应显著。关税影响尚属可控

苹果Q3遭遇8亿美元关税成本,预估Q4将升至11亿美元,但部分用户提前购机,有效对冲压力,库克估约1%营收来自此提前需求。中国市场转正回温

大中华区销售年增4%,达153.7亿美元,结束连续两季下滑,受惠于中国官方补贴计划对iPhone销售的支撑。AI投资大幅扩张

库克强调AI为「我们这个世代最深远的科技」,苹果将显著增资AI,已并购7家公司,未来也将更积极考虑战略性并购以强化布局。软体与服务维持稳定成长

服务营收达274.2亿美元,年增13%,App Store与iCloud贡献明显;但iPad与穿戴装置部门表现疲软,分别下滑8%与8.6%。

major news item closely

general manager Daryl

U.S. inflation heats up in June, tariffs push up the prices of imported goods, and Federal Reserve interest rate cuts are delayed

In June, the U.S. PCE price index increased by 0.3% month-on-month and 2.6% year-on-year. Core inflation remained at 2.8%. Among them, the prices of imported furniture, entertainment supplies, clothing and other commodities increased significantly due to the increase in new tariffs. Although energy prices rebounded, service prices remained stable. The rebound in inflation has turned the market's expectation of a September interest rate cut by the RSC, which may be extended to October or later. Consumer spending growth remained at 0.3%, but a slowdown in the labor market and a flat savings rate indicate that future spending momentum may face challenges.

Inflationary pressures are rising again, coupled with President Trump's new wave of tariff policies, both companies and consumers will face higher cost pressures, which may disrupt economic growth and monetary policy in the third quarter.

关税效应明显推升商品价格

耐久财如家具、娱乐用品价格分别上涨1.3%与0.9%,为逾一年来最大涨幅,显示新关税政策已开始对消费市场造成影响。核心PCE通膨维持高位

排除能源与食品的核心PCE月增0.3%,年增2.8%,远高于联准会2%目标,加大延后降息可能性。消费支出温和复苏

消费支出月增0.3%,为Q2 GDP增长3%提供支撑,但实质支出仅小幅增长0.1%,反映通膨侵蚀实质购买力。劳动市场略显疲态

初领失业金人数小幅增至21.8万人,续领人数高达194.6万人,显示企业在关税不确定性下保守增聘。储蓄率未提升,预示消费压力

6月个人储蓄率维持4.5%,薪资年增率实质放缓至0.9%,中高收入家庭亦开始出现财务压力迹象。

Trump has significantly adjusted his tariff policy, imposing a 40% tariff on transshipment goods, impacting global supply chains

U.S. President Trump signed an executive order on July 31, 2025, re-establishing so-called reciprocal tariffs on imported goods from dozens of countries, with rates ranging from 10% to 41%, and imposing an additional 40% tax rate on all goods that are transshipped through third places to circumvent tariffs. This wave of tariff adjustments has put pressure on major trading countries including Canada, India, Taiwan, and Brazil, and has also affected a series of bilateral negotiation processes and market reactions in the next 90 days.

Although the United States has reached preliminary agreements with the European Union, Japan, South Korea, etc., the 35% punitive tariff on Canada and the 25% tax rate on India show the highly political nature of Trump's trade policy. Although the market has already expected the "Trump Always Chickens Out" model, it still needs to closely observe the real impact of subsequent inflation and corporate profits.

关税调整幅度大、针对性强

川普最新行政命令设定10%至41%之间的「对等关税」,对加拿大商品课35%,印度25%,台湾20%,巴西实施堆叠后的总税率达50%。转运货物面临惩罚性关税

为打击透过第三地转运规避关税的行为,白宫宣布对所有经第三地转运的货物加征40%额外关税,将对全球供应链造成重大影响。加拿大与墨西哥处境不同

加拿大因宣布支持巴勒斯坦建国,触怒美方,关税升至35%;而墨西哥则获得90天关税暂缓,显示政治外交立场成为关键变数。市场反应尚称温和

受益于南韩、日本等已达成协议,与墨西哥暂缓,欧洲与亚洲股市期货仅小幅回落。分析师指出市场已认知川普政策具可逆性与谈判空间。国际政经风险升高

各国反应不一,加拿大与巴西表态强硬、泰国与台湾则寻求谈判缓冲,川普模式再度突显全球政经的不确定性与美国单边主义的强势运作。

Disclaimer: The views in this article are from the original Creator and do not represent the views or position of Hawk Insight. The content of the article is for reference, communication and learning only, and does not constitute investment advice. If it involves copyright issues, please contact us for deletion.

_918574176_642.jpeg?w=3840&q=100)

![[Pre-market analysis of U.S. stocks] U.S. stock futures rise, investors expect rebound (2025.08.04)](https://hawk-oss.hawkinsight.com//picture//202508/328687551_275.png?w=3840&q=100)

![[Intraday Analysis of U.S. Stocks] Technology and semiconductors led the decline, major U.S. stocks fell (2025.10.23)](https://hawk-oss.hawkinsight.com//picture//202508/328826217_1.png?w=3840&q=100)